In the world of finance, the relationship between investors and accountants has always been a complex one. Investors depend on the financial statements prepared by accountants to guide their investment decisions, but what happens when the language of accounting changes? Over the past couple of decades, the International Financial Reporting Standards (IFRS) have undergone significant transformations, shifting from historical cost accounting to an emphasis on fair value. This transition raises important questions about the reliability of financial metrics and how investors interpret them.

Understanding the Shift to Fair Value Accounting

Historically, accounting practices relied heavily on historical cost, where assets and liabilities were recorded at their original purchase price. This approach provided a stable and consistent basis for evaluating a company’s financial position. However, as the financial landscape evolved, regulators began to recognize the limitations of this method. The IFRS has progressively incorporated fair value measurements, a practice that aims to reflect the current market value of assets and liabilities.

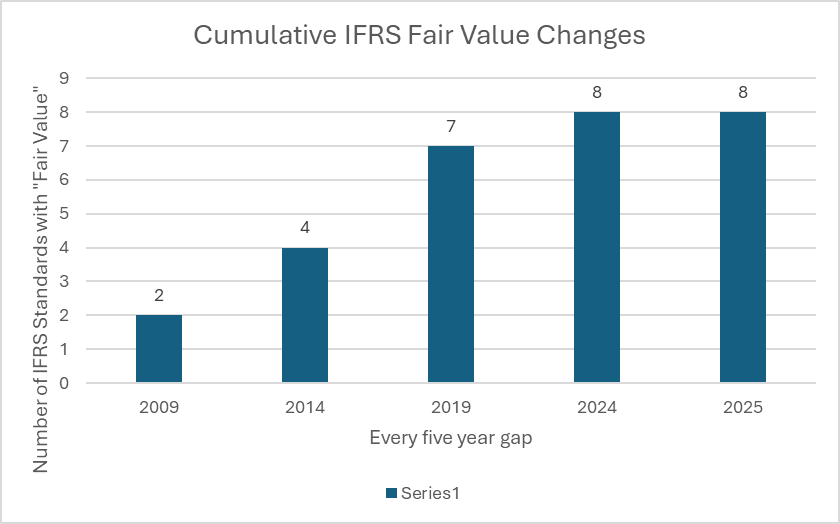

The trend toward fair value accounting has been notable over the last 25 years, with an increasing number of IFRS standards requiring fair value assessments. This shift is not just a minor adjustment; it fundamentally alters how financial statements are structured and interpreted. For instance, from the mid-2000s to 2019, the number of IFRS standards necessitating fair value evaluations reportedly doubled approximately every five years. Such rapid changes could lead to a disconnect between the information that accountants provide and the expectations of investors.

Key Points to Consider

1. **Impact on Financial Ratios**: Traditional investment metrics such as the Price-to-Book (P/B) ratio and Price-Earnings (P/E) ratio may no longer provide the insights they once did. If book values are inflated due to fair value adjustments, a low P/B ratio might suggest an undervalued stock when, in reality, the book value may not reflect the true economic value of the company.

2. **Earnings Distortion**: Earnings figures can be misleading as well. Fair value adjustments that flow through profit and loss statements may distort the earnings reported, making it difficult for investors to gauge a company’s true performance. This raises concerns about the reliability of earnings-based measures for decision-making.

3. **Cash Flow Considerations**: Investors often turn to cash flow statements for clarity. However, changes introduced by IFRS 16 complicate this. This standard requires lease payments to be split into interest and capital portions, altering the way free cash flow is assessed. Such changes can further obscure the financial health of a business.

4. **Value Perception**: There may be a discrepancy between how accountants perceive value and how the market does. A company could have a seemingly attractive low P/B ratio due to inflated net asset values, yet the market may undervalue it based on its cash flows and earnings.

Investor Insights: Adapting to New Financial Realities

For investors, the implications of these changes are profound. The very metrics used to evaluate investments could be losing their effectiveness. Here are a few insights for navigating this new landscape:

– **Rethink Investment Metrics**: Investors should reevaluate the weight they give to traditional financial metrics. Understanding the underlying assumptions and adjustments made in financial statements is crucial for making informed investment choices.

– **Focus on Cash Flow**: Given the potential distortions in earnings and book values, a closer examination of cash flow statements can provide clearer insights into a company’s operational performance.

– **Stay Informed**: Keeping abreast of changes in IFRS and their implications for financial reporting is essential. Investors who understand how accounting standards affect financial statements will be better equipped to make sound decisions.

– **Engage with Analysts**: Collaboration with financial analysts who specialize in interpreting financial statements can provide additional insights. These professionals often have a deeper understanding of the nuances in accounting standards and can help investors navigate the complexities.

Conclusion

The shift from historical cost to fair value accounting in IFRS represents a significant evolution in financial reporting. While this change aims to provide a more accurate picture of a company’s financial health, it also presents challenges for investors who rely on traditional metrics. As the landscape continues to evolve, it is imperative for investors to adapt their strategies, focus on comprehensive analysis, and remain informed about the implications of accounting standards. By doing so, they can navigate the complexities of financial reporting and make more informed investment decisions in an ever-changing market.