The recent fluctuations in share prices of banks listed on the Johannesburg Stock Exchange (JSE) have sparked extensive discussions among investors and analysts alike. Particularly, Capitec Bank has emerged as a focal point due to its impressive performance numbers, yet its stock trades at a valuation that raises eyebrows. This blog post aims to peel back the layers of bank valuations, exploring what truly underpins these figures and what investors should consider when evaluating these financial institutions.

To understand the valuation of banks such as Capitec, we must first grasp the fundamental nature of banking itself. At its core, a bank operates as a financial intermediary, facilitating the flow of capital between savers and borrowers. While many might think of banks as simply institutions with grand offices and sleek branding, the essence of a bank lies in its ability to secure low-cost capital. This access allows banks to lend money at higher interest rates, creating a profit margin known as the interest spread.

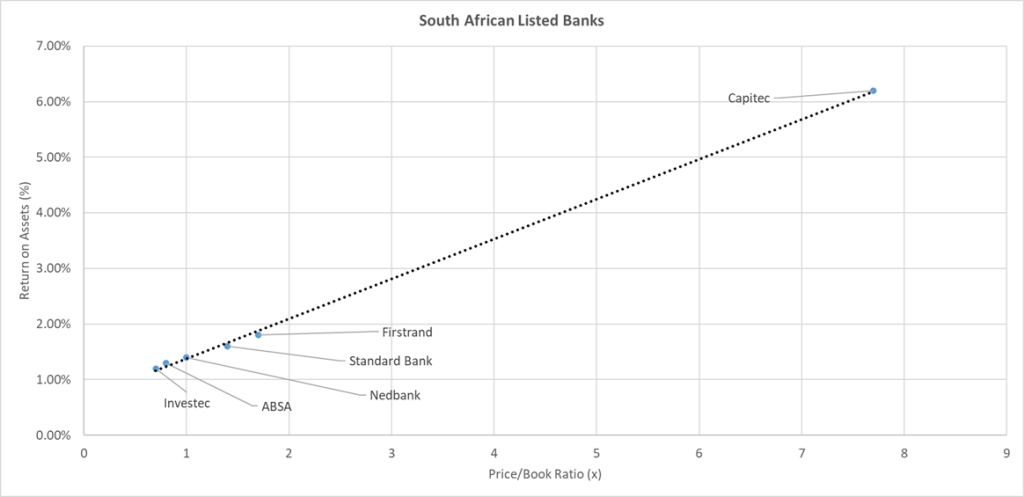

Banks primarily generate revenue through this spread, which means that the efficiency and effectiveness with which they utilize their balance sheets are crucial to their profitability. Thus, when evaluating a bank’s stock price relative to its book value, it’s essential to consider how well that bank is leveraging its resources to generate returns. Capitec, for example, is currently trading at a Price/Book ratio of 7.7, which is substantially higher than the average of 1.1 for its JSE-listed competitors. This considerable premium raises questions about its valuation.

When assessing whether Capitec is “expensive,” we must look beyond the raw numbers. Instead, we need to analyze the bank’s return on assets (ROA) in relation to its Price/Book ratio. A scatterplot of these two metrics for local banks reveals a compelling picture: the valuation of these banks aligns closely with their performance in deploying their balance sheets. This means that while Capitec may appear costly based on its Price/Book ratio, its efficiency in generating returns could justify this valuation.

Conversely, other banks like ABSA trade at a much lower Price/Book ratio of 0.8. The question then arises: Is ABSA undervalued, or is Capitec merely overvalued? The answer is not straightforward, as various factors play a role in the valuation equation. Additionally, it is worth noting that banks like Investec and Firstrand have significant international operations, particularly in the UK, which complicates direct comparisons due to differing economic performance metrics across regions.

As investors and traders analyze these banks, it’s crucial to understand the potential for valuation shifts due to changes in profitability or broader economic conditions. For instance, if Capitec’s profitability were to decline, we could expect its high valuation to adjust downwards. Conversely, if less profitable banks identify efficiencies and improve their returns, their valuations may experience upward re-ratings.

Moreover, external economic factors, such as interest rate movements or shifts in consumer credit risk, can significantly impact the entire banking sector. For example, a rising interest rate environment could benefit banks that can charge higher rates on loans, while simultaneously increasing the risk of loan defaults. These dynamics underline the importance of considering not just historical data but also future projections when evaluating bank valuations.

Key takeaways from this analysis include the significance of understanding how banks utilize their capital, the necessity of comparing performance metrics like ROA to Price/Book ratios, and the potential for environmental changes to influence bank valuations. As such, investors should remain vigilant and adaptable, continuously monitoring both individual bank performance and the overall economic landscape.

In conclusion, while Capitec may appear expensive relative to its peers at first glance, a deeper examination reveals that its valuation could be justified based on its performance metrics. Conversely, investors should not overlook the potential of other banks that may be undervalued in the current market context. As the financial landscape evolves, both traders and investors will need to reassess their strategies, ensuring they remain informed about the factors that drive bank valuations and the overall health of the banking sector. Engaging in this sort of critical analysis will empower investors to make more informed decisions, ultimately leading to better outcomes in their investment portfolios.